The Differences between Individual, Group, Medicare and Medicaid Insurance

There are several forms of health insurance, and you can agree on an insurance package with

an understanding of each of them. Community, patient, Medicare and Medicaid insurance are

the most popular forms of insurance.

Group Health Insurance

The health insurance group is supported by an employer, agency or union. The arrangement

between the employer and an insurance firm that operates group arrangements makes this

possible. The group insurance policy offers a group of people which typically allows for a

discount. Employers who cover companies pay usually a part or all of the premiums. Employees

shall pay the remaining premium and the premium due will generally be taken off the top of their

salary check per pay period.

Employers can select between a variety of plans, including management and benefits, or only

one form of plan can be provided. Many community programs also provide incentives for dental

and vision.

Group plans provided by unions, clubs and associations are comparable to company plans by

encouraging the party to obtain a discount. However, they vary since each person pays his or

her own premiums absolutely

Both employers and workers may benefit from group programs. As a tax expenditure, employers

can say premiums charged. The discount and/or reimbursement for some of the premiums is

given to workers which results in very inexpensive health benefits. Such plans will also have

more money coverage than most individual plans.

Individual Insurance

You will subtract your health insurance premiums from your federal taxable income if you work

as a self-employed individual. This helps reduce the pressure a little and allows you as a

company owner to get decent health insurance. You may also subtract insurance premiums for

the whole family. See how this plays for your accountant.

You should buy individual insurance if the company does not have medical coverage. You may

pick the business you want to run and the type of package that best fits your needs with

individual insurance. To find the best package for you, you can buy around and compare prices,

benefits, deductibles and payment plans. Unfortunately, the whole premium is expected to be

charged and community discounts are not given.

Indemnity or Managed Care Plans

If you have a group plan or an individual policy, these two forms of policies also give you

options. You can choose between insurance and treatment plans. In some ways they are

similar, but in others they are very different. Both plans provide a broad variety of facilities

including medical, hospital and surgical facilities. Many of these plans provide some form of

limited dental and/or vision coverage for prescription drug coverage.

You can select a physician for medical treatment with health benefits and even change

physicians if you wish. This form of plan may allow you to pay a deduction. You could also face

higher out-of-pocket costs. With managed care, the option of some network providers, known as

network providers, will save you money. For any office visit you will have a co-pay rate like $10

or $20. Prescription medicine is graded as type and non-form, with lower cost forms protected

by the insurance. The health maintenance organization (HMO), the preferred provider (PPO)

and point-of-service (POS) plans are three types of management health care plans.

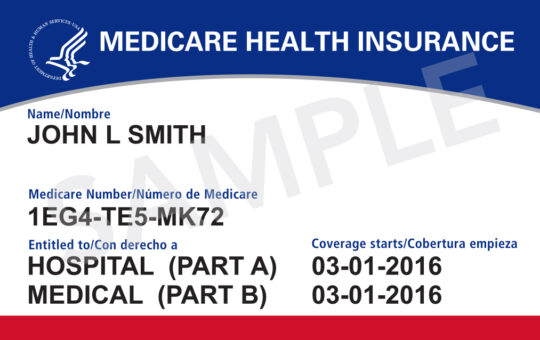

Insurance for Medicare

Medicare Insurance is a scheme given to elderly people 65 years of age by the federal

government. Medicare coverage may also be available to eligible persons with a disability or

end-stage renal disease (ESRD). Medicare is composed of four parts: Part A, Part B, Part C and

Part D. Section B is physicians ‘and other associated providers’ medical insurance. Part C or

Medicare Advantage is a program which provides individuals with a private health plan for the

benefit of Part A, B and D. Section D is a medical treatment prescription.

Part A needs no premium because payroll taxes have been charged in the years of a worker.

Part B asks for a monthly income premium. Part D still requires a premium, but if you are not

enrolled as soon as you apply for Medicare, this premium is higher. For those with Medicare

Medigap provides private insurance to aid with paying costs not covered by Medicare.

Insurance for Medicaid

A federal-state system provides for Medicaid benefits that each state has its own rules on

covered costs and eligibility. For those with small incomes, pregnant women and their newborn

children and blind or disabled people, medicaids are available. Children may also be protected

by certain circumstances, even if the parent is not exempt. You should review the criteria with

your Medicaid office.

Such insurance types vary in many respects and cover a range of persons and situations. They

are distinct. Study every form carefully to see what works for you.

Life & Disablity Insurance for Employees

by admin

Why Long-Term Care Insurance should be part of your portfolio

by admin

The Basics of Medicare

by admin

Why Long-Term Care Insurance should be part of your portfolio

However, a real crisis is now underway. When the U.S. population ages and a tidal wave of baby

boomers hits retirement age, seven of these boomers will soon be confined to a nursing home or

an assisted living facility. The average annual cost of nursing home treatment is $250,00, and

Medicaid charges little on nursing home care. This leaves most seniors with two options: selling

their assets and paying bills based on Medicaid, or maintaining assets with long-term insurance

policy.

A long-term care package is available to someone who is 55 years of age or older and designed

expressly to cover the costs of nursing home isolation or assisted living. Long-term care plans

may be obtained individually or, according to financial advisor Steven Daar, as a life insurance

brace. Long-term care levels differ based on the applicant’s age , gender , health background and

lifestyle. The patient who has a greater risk of incurring an illness that will put him or her in a

nursing home and who applies for insurance at a higher age would have a premium higher than

the patient with little health problems who applies at age 55.

Long-term care needs will bankrupt even seniors who are most prepared. This will take a

portfolio of $2.9 million, producing 3.5% of income just to fund one year of nursing home

treatment at today’s $100,000 annual expense. Many retirees struggle to invest in an IRA or

401(k) account. A retired person who is single without dependents and does not intend to give

his or her assets to a partner, relative or organization may choose to invest what they have and

then apply for Medicaid. Medicaid eligibility requirements vary from state to state, and

navigating the fine print road to acceptance also requires an elder lawyer’s assistance.

Nevertheless, a disabled person who is married, who has children or who wishes to move his or

her assets to a charity should have a long-term care policy to protect those assets and the existing

living needs of his or her spouse.

Georgia health care advocate Cindy Holtzman argues that the presence of filial obligation laws in

30 states is an important concern for the elderly with grown children. A child is responsible for

the nursing home bills of his or her parent if the parent can not pay. While such laws have been

widely ignored in the past, the increasing cost of nursing home treatment combined with cuts in

Medicaid funding has prompted nursing homes to start implementing such laws and file civil

suits against indigent parent children. For example, in the state of Pennsylvania, a daughter was

sued for their care by a nursing home for over $300,000. The home lost the lawsuit so the

daughter had to hire an attorney to prove she couldn’t afford the charge. Many states, such as

Ohio and Massachusetts, can prosecute adult children who refuse to provide long-term care for a

parent. These charges can result in either a fine or imprisonment, and would appear on criminal background check. The harm to the parent-child relationship following participation in one of

those cases that outweigh the actual financial loss, but both can be avoided by buying a

long-term care policy.

Many financial planners advise postponing long-term care insurance purchases well after

retirement age, but it may be wise to start shopping before retirement. Most insurance providers

are withdrawing their long-term care plans, and those insurers currently providing long-term care

plans are raising premiums significantly. Insurance firms make money by paying premiums to

invest in debt or money market securities, and then from the income stream they earn from

interest and dividend payments. Despite interest rates for Treasury bonds running above 3% and

financial markets charging less than 1%, these companies are losing financial on long-term care

policies. Despite growing competition for long-term care plans, there could be less insurers to

choose from. High demand combined with small supply implies high commodity costs.

Any type of insurance is the last thing that someone wants to buy, but as life’s seasons change, so

will life’s demands. A worry-free retirement starts with sound financial planning, which will

include long-term care insurance.

The Basics of Medicare

Since every year the federal government makes changes, many people find Medicare hard to

grasp. Do you need something? What is it covering? How much does it cost? When and how do

you subscribe? Although the program does have thousands of questions, most of the answers are

clear.

When do I apply to Medicare?

annual review process. It can be especially effective to shop for your auto insurance policy once

a year, when growing numbers of insurers use competitive pricing and analyze their customer

behavior when setting rates.

Believe it or not, in order to apply for Medicare you don’t need to be just 65 or older. Anyone

who is under 65 can also sign up. Those under the age of 65 should also be disabled. Individuals

of any age with end – stage renal failure are also eligible for Medicare.

How Can I Sign Up?

You will automatically receive sections (A and B) of Medicare on the first day of the month you

turn 65 when you receive Social Security or Railway Retirement income. Many that are 65 who

are disabled will be automatically enrolled in the system after 24 months of obtaining disability

payments from the Social Security or Railroad Retirement Board. You can then receive your

Medicare card in the mail 3 months before your 65th birthday, or on the 25th month after being

disabled.

You will sign up for those who do not already earn Social Security or Railroad retirement

pension. You can do this by contacting the Board of Social Security or the Railroad Retirement.

Those with renal disease in the end stage will also contact social security to apply for benefits.

What Is Medicare Covering?

Medicare is composed of 4 parts: A, B, C and D. This lets you choose which covers are better for

you. Bear in mind that you could be subject to a penalty or have to wait to sign up for that

particular type of coverage if you refuse either of these coverages without some form of health

insurance.

Part A is coverage from the hospital. It will also fund hospital services inpatient, skilled nursing,

home health care, and hospice care.

Part B is treatment by the medical or doctors. It would also offset the cost to doctors as well as

long-lasting medical equipment, diagnostic testing, preventive treatment and recovery therapy.

Part B can also help to cover supplies for diabetes.

Part C is made up of Medicare Benefit Plans. These services are issued by private insurance

firms. Often bundle Part A, Part B and occasionally Part D benefits into one kit. The Medicare

Supplements are an alternative to Medicare Benefit Plans.

Section D is the distribution of the prescription medications. The type of prescription drug

coverage varies from state to state but it can help offset the cost of your medications, supplies of

medication, and some vaccines. Part D plans are provided by private insurance companies, or

you can get one through a Medicare Advantage plan which offers them.

How much does it cost to My Medicare?

With other health insurance policies, you are subject to copayments, premiums, deductibles, and

coinsurance fees. Any part of Medicare has related costs to it.

For Part A, there are no premiums as long as you paid enough in Medicare taxes while you were

employed. The remainder of the cost depends on the sort of service you offer. For example, if

you are admitted to hospital, you must fulfill a deductible of $1,184 for each benefit period in

2013. When the limit is met, you won’t be spending anything at the hospital for the first 60 days.

If you’re stuck in hospital for 61 to 90 days, you’ll have to pay $296 a day per duration of gain.

You’ll have to pay $592 a day from day 91 to date 150. You will be responsible for all expenses

associated with your stay at the hospital until you pass it. Also keep in mind that there are regular

charges for skilled nursing services and home health care.

For Part B coverage, most people would pay $104.90 per month as a premium. Some people pay

higher primes depending on their level of income. You subtract this number from your social

security benefits. In 2020 there’s also an $144.60 annual limit. You must pay 20 per cent

coinsurance for most of the facilities under Section B.

What you’ll pay for Part C varies from plan to plan. There are some plans which cost nothing.

Another would cost hundreds of dollars. The same holds true for your coverage for Part D.

Knowing Medicare can be a challenging job. Choosing the best coverage may also be equally

daunting. Maybe you have more Medicare concerns or issues that have not been addressed here.

If so, there’s plenty of other available tools. For those interested in learning about the system

online, Medicare.gov is the official government website. You can even chat over the phone to

someone who works at Medicare. To reach them the number is 1-877-486-2048

Life & Disablity Insurance for Employees

Compare Life Insurance for Employees to Find Big Business Benefits

A group life insurance policy is a life insurance plan intended to protect a wide

number of individuals under a single policy. For a group insurance policy, the

policy provider is the company or employer, and the policy offers benefits to an

entity’s members and/or workers. Compared to an individual policy coverage.

Group Employee Insurance benefits

Group or Employer Insurance Provides a full coverage insurance policyMembers or employees will retain insurance plans, for as long as they remain

with their group or company. For individuals who can’t afford to purchase a stand

alone policy, group or employee insurance is a great alternative that can save

money in the long run.

Premium competitive prices

A group insurance plan’s premium rates are more affordable compared to the

general stand alone individual life insurance plan. This is because the risk

percentage is distributed equally across the whole group. Generally speaking,

the premium amount is split between employees and employers and is 30-35 per

cent more economical than individual life insurance plans. Besides that, there are

numerous other variables that decide the policy’s premium rate such as

occupational risk, average age group, etc.

Provides support for the families of workers

A group insurance package offers protection for the insured ‘s relatives. So if you

own a group insurance package then you shouldn’t need to shorten your budget

by getting your family members a separate life insurance policy. Most group

insurance plans provide comprehensive support to the insured ‘s family i.e. the

spouse and children.

Effortless option to pay

A workplace compensation benefit premium is deducted directly from the bank

account or from the employee’s wages. And the premium payment process is

quick and trouble-free. In addition it automatically reduces the risk of missing the

premium payment due date.

A disability means being unable to perform the duties of your work with fair

consistency during the waiting period due to sickness, accident or pregnancy and

for the first 24 months that you seek LTD benefits.

Disability Definition

You are deemed partially impaired during this time if you work but are unable to

earn more than 80 percent of your measured pre-disability earnings. After that,

you are deemed partially disabled if you are unable to perform with fair

consistency the duties of any job for which you are fairly competent through

schooling, training , or experience as a result of illness, injury, or pregnancy

You are deemed partially disabled at some stage after the first 24 months if you

work but are unable to earn more than 60 percent of your adjusted earnings for

pre-disability in that profession and in all other occupations for which you are

fairly qualified.

LTD Insurance helps cover your finances in the case of an injury or disease.

When you participate in LTD coverage, if you are disabled it will pay you a

percentage of your monthly earnings.

Determining if Pet Insurance is Worth It

You have checked and made sure your animal is either spayed, neutered or up-to-the-date with

all its vaccines, but as we all know, we should do more to make the best friend of man the

healthiest. You may end up facing a huge bill when your furry friend gets sick or hurt. You may

think of pet insurance, but you don’t know if your monthly budget is worth the additional cost.

Review some information about pet insurance to help you determine if it is suitable for your

financial plan.

How Medical Professionals have evolved in the Pet Industry

Most of the veterinarians were medical professionals at one time, from diagnosis to surgery in

hospitals or even house calls. Some small animals — particularly dogs and cats — were trained,

while others, especially in rural areas, were looking after livestock.

Pet insurance deductibles are available, much like human insurance. There are also

payment limits on specific treatment types, and exclusions for certain conditions. You

pay a premium for your selected coverage, and you have an assigned deductible that

directly impacts the premium you pay.

Average Vet Bill Cost

Cancer and heart failure, worth thousands of dollars to manage, are two of the most costly

canine illnesses. Hip dysplasia, which sometimes involves service, can last up to six thousand

dollars. The bloat of the stomach may cost between $1,500 per incident and $7,000. This can

range from handling poison intakes to conducting operations to extract an external entity.

Cat veterinary costs are normally lower but often overdrive the family budget. Bladder stones

and oral surgery, both averaging over $900 for treatment, are common problems. The cats also

get specific cancer types that cost up to $1,500 for care and up to $3,000 per eye for cataracts.

Average Rate for Pet Insurance

The average price of pet insurance is $32 for dogs and $22 for cats as of 2015, according to

PetInsuranceQuotes.com, a U.S. independent pet insurance provider, from 2015. The

environment you live in and the age, health and natural life influence the price of your product.

The average German Shepherd is $39 a month due to hip dysplasia tendencies.

About $44 a month for boxers who are susceptible to cancer. The lowest insurance premium

mixed breed dogs is $28 a month. Cats are all around less costly, but exceptions exist. Persian

people are prone to respiratory problems and have an average of $29 a month for benefits.

How Pet Insurance operate in Everyday Life

Pet insurance will, based on the plan and the provider you choose, reimburse you for up to 90%

of your overall veterinary costs. The veterinarian shall be charged beforehand and a petition

shall be made. Policies for injuries and diseases are necessary and incidents only. You should

apply to a daily treatment rider to cover frequent checks, vaccines and spells and neutrals. The

latter plan may not be worth it if your pet is spread or neutered already.

Also important is pet insurance, which typically has deductibles between $100 and $1,000. The

higher the threshold, the lower the coverage. The waiting period is as fast as you can and the

amount you can receive during a 12-month span is calculated by the annual cap. Regardless of

the scheme, intend to budget an external emergency fund to cover up-front expenses.

Popular exclusions and Pet Insurance Limitations

by admin

What To Look For When Buying Pet Insurance

by admin

What To Look For When Buying Pet Insurance

by admin

Pet Insurance for Large Dogs

Is Pet Insurance For Your Large Dog a Good Idea

When you have a big dog and are considering buying pet insurance, there are a range of

issues to remember.

Drawbacks to Insuring a Large Breed Dog

Animal insurance operates much like human insurance; in case of sickness, you pay a fee

and get compensation to protect your animal. The insurance provider pays out the

medical expenses in the event of a claim.

Pet insurance deductibles are available, much like human insurance. There are also

payment limits on specific treatment types, and exclusions for certain conditions. You

pay a premium for your selected coverage, and you have an assigned deductible that

directly impacts the premium you pay.

Another concern is that large dogs are usually very physical, they need exercise to remain

healthy and they are more susceptible to accidents. Many plans will introduce up to 20

per cent surcharge to cover a big dog

Assessing the risk factors of Large Dog Breeds

In determining whether or not you want pet insurance, you have to weigh the

disadvantages against what you know about your pet, and what it will cost in an

emergency to take care of. Of example, if your dog breaks a leg, it’ll cost as much as

$2,500 in vet bills. Balance it against your annual insurance premium costs.

Other risk factors such as your dog age, activeness and or maintain of control when in

public. Answering these questions will help you determine the risk factors, and get an

idea of how to treat an unexpected illness or accident.

Another concern is that large dogs are usually very physical, they need exercise to remain

healthy and they are more susceptible to accidents. Many plans will introduce up to 20

per cent surcharge to cover a big dog.

Until enrolling, it’s important to know and understand what variables, such as the

breed of your pet and any pre-existing conditions, that affect coverage. Check

out how much the price will go up, and why. Ask whether your premium would be

affected by the amount of claims you make. When you’re confused about the

wording of the contract, contact the pet insurance company and ask Customer

Service to clarify it in a way that you can clearly understand.

Exclusions in pet insurance policies can have a major impact on the coverage of big dogs,

and insuring a big dog is typically more expensive than insuring a small dog, but pet

insurance in the event of a catastrophic illness and injury still has advantages.

Medical expenses have also skyrocketed for animals, and if you can not afford a large vet

bill, coverage may mean the difference between life and death for your pet.

Speak to your doctor about the wellbeing of your pet and ask for advice on it. Do not

forget to contact your nearest humane society if you want to buy insurance. And be a

smart shopper. The insurance rates for animals vary from carrier to carrier, so shop

around.

Popular exclusions and Pet Insurance Limitations

by admin

What To Look For When Buying Pet Insurance

by admin

What To Look For When Buying Pet Insurance

by admin

What To Look For When Buying Pet Insurance

Overview of Animal Health Insurance Companies and Policy Coverages

Pets enjoy a longer lifespan, thanks to advances in health care and quality food

goods. There’s also a rise in the cost of keeping a pet: food, toys, accessories

and health care add up.

A pet insurance policy will help you plan treatment for your pet — and cover the

expense of daily care, accidental accidents and illnesses.

annual review process. It can be especially effective to shop for your auto insurance policy once

a year, when growing numbers of insurers use competitive pricing and analyze their customer

behavior when setting rates.

Compare pet insurers if you want to enroll your pet into a pet insurance policy.

The variations in rates, costs , benefits, co-payments, sample refunds, and

product specifics, including exclusions and other features, are seen in the

comparison side by side.

Look at the pet insurance provider’s record of reliability. The trick to choosing a

pet insurance carrier you can depend on. Always go with the provider that has

proven reliability, expertise, and advice.

How long was the provider in business? Are they financially trustworthy? How

many policies do they still have in force? Will they have professional

veterinarians who know the needs of the pets and help in designing policies?

Some pet health insurance policies that exclude pre-existing, genetic, congenital,

or breeding-related conditions, and may impose limits on your coverage when

you submit a claim.

Until enrolling, it’s important to know and understand what variables, such as the

breed of your pet and any pre-existing conditions, that affect coverage. Check

out how much the price will go up, and why. Ask whether your premium would be

affected by the amount of claims you make. When you’re confused about the

wording of the contract, contact the pet insurance company and ask Customer

Service to clarify it in a way that you can clearly understand.

Would you want coverage for documented routine health (vaccinations, flea and

heartworm control, wellbeing exams and evaluations), unexplained medical care

(chronic diseases, surgery and hospitalization, medications, assessments,

laboratory testing, illnesses , injuries) or full coverage treatment that covers

inherited disorders and health?

Discuss the health of your pet with your veterinarian, get an idea of what specific

health conditions your pet may face and could be linked to the breed, or whether

there is a history of health issues in the family tree of your pet. More about the

Top 10 Reasons Pets Visit Vets can also be learnt.

Want to be ready for an emergency or unexpected illness? Now is the time to

decide so that once your pet begins to age you won’t find yourself unable to

receive coverage due to a pre-existing condition.

2 Reasons to Call your Auto Carrier after your Honeymoon

Your car insurance company isn’t necessarily the first person you want to contact after you’re

married, but they will be on your personal list as soon as you go back from your honeymoon.

You will not only need to add the name of your partner to the policy, but you may also be

eligible for a car insurance discount when you tie the knot. Most automobile insurance firms give

lower rates to married couples than individuals pay and this trend has some historical foundation.

Better married couple rates

Nobody knows exactly why, but married couples appear to be in fewer traffic accidents — and

therefore file less claims — than their counterparts. Perhaps settling and raising children is a

prudent rider, or maybe married couples prefer to live in less trafficked neighbourhoods.

Whatever the reason, insurers are able to offer lower rates to married couples because they are

less likely to lose insurers money.

annual review process. It can be especially effective to shop for your auto insurance policy once

a year, when growing numbers of insurers use competitive pricing and analyze their customer

behavior when setting rates.

Checking your savin

The savings would depend on many factors, including the state, the insurance provider and

individual risk factors ( e.g. age , gender and driving records). Call the insurance provider to ask

them to get new car insurance rates and see how much you can save. You won’t only be able to

cover your pension from your savings, but you can pay off your monthly premiums for a few

Page 1 of 2

bucks.